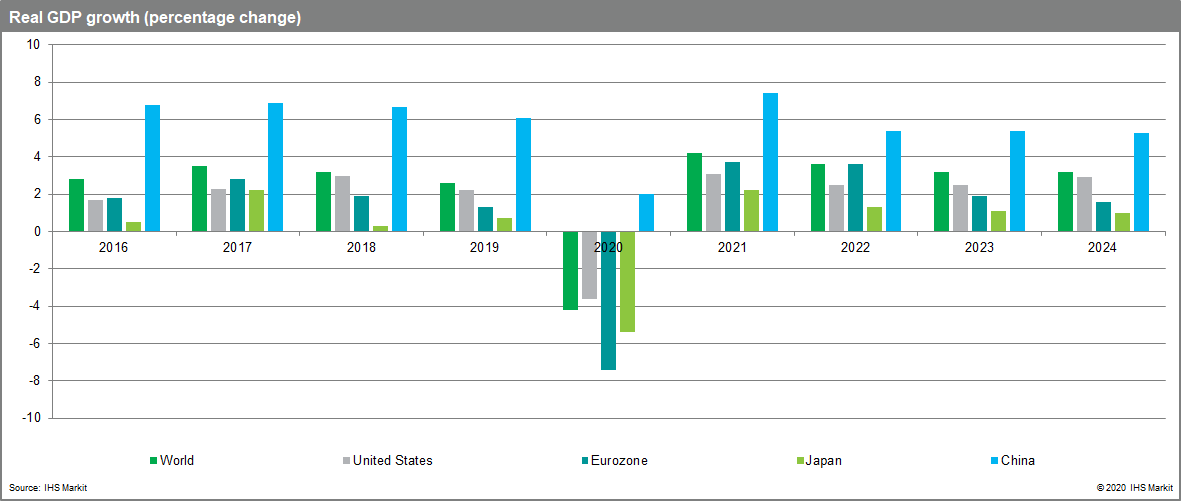

US economy decelerates, mainly due to delta and supply chains

The headlines last week reported a significant deceleration in US economic growth in the third quarter. Yet it is not likely that this reflects a new trend in demand. Rather, there is considerable evidence that the slowdown was due to two important factors: supply chain disruption and the outbreak of the delta variant of the virus. For now, the delta variant is abating. In addition, there is reason to expect that supply chain disruption will wane over time as demand for goods lessens and supply constraints in Asia ease.

In any event, here are some details: Real GDP increased at an annualized rate of 2.0% from the second to the third quarter. This was a substantial deceleration from the 6.7% growth in the second quarter. The biggest change from the previous quarter was a sizable shift in consumer spending on goods. Having grown at a rate of 13.0% in the second quarter, goods spending fell at a rate of 9.2% in the third quarter. Moreover, this was mainly due to a decline in spending on durable goods that fell at a rate of 26.2%. In addition, that decline was largely driven by a big drop in purchases of automobiles. The latter was likely due to the shortage of semiconductors which is disrupting supply chains in the industry.

Despite the sharp decline, real spending on automobiles remained 5.2% above the pre-pandemic level in the fourth quarter of 2019. Overall consumer spending on goods was 15.2% above the pre-pandemic level. Thus, even as goods spending declined, the level of spending was unusually high, thereby contributing to supply chain stress and rising prices.

Although consumer spending on services continued to grow in the third quarter, it decelerated sharply from 11.5% growth in the second quarter to 7.9% in the third quarter. There was an especially sharp deceleration in spending at restaurants—indicative of the effect of the delta variant on social interaction. Overall spending at restaurants remained below the pre-pandemic level.

If spending on automobiles and restaurants had grown in the third quarter at the same pace as in the second quarter, then real GDP would have grown at a rate of 6.6%—almost the same as the second quarter. Thus, the sharp deceleration in GDP growth can largely be attributed to supply chain disruption and the impact of the delta variant.

As for business behavior, investment in equipment fell at an annual rate of 3.2% while investment in structures fell at a rate of 7.3%. These declines were more than offset by a sharp 12.2% increase in investment in intellectual property. Thus, overall business investment increased at a modest pace of 1.8%. Business investment in inventories increased strongly, offsetting the decline in the previous quarter. Residential investment fell at a rate of 7.7%, slower than the decline in the second quarter.

Both exports and imports of goods declined in the third quarter. However, imports of services increased sharply. Overall, trade made a negative contribution to GDP growth. Finally, Federal government purchases fell sharply in both the second and third quarters as fiscal support for the economy waned. If the US Congress passes the infrastructure bill now under consideration, this will likely have a positive impact on purchases in the quarters to come. State and local spending increased at a healthy rate of 4.4%.

Regarding inflation, the GDP report provided evidence that inflationary pressures are abating. The personal consumption expenditure deflator (often call PCE-deflator), which is the favorite measure of inflation of the Federal Reserve, increased at an annual rate of 5.3% in the third quarter, a deceleration from the 6.5% increase in the second quarter. Interestingly, and not surprisingly, the price index for consumer durable goods was up at a rate of 9.6% in the third quarter while the index for consumer services was up at a rate of 4.2%. In other words, prices rose strongly in the category that was most disrupted by supply chain problems. This offers hope that, when supply chain issues are resolved, inflation will decelerate. That, in fact, is one of the arguments suggesting that current inflation will turn out to be transitory.

US consumer spending shifts in a new direction

The US government reported that personal income declined in September but spending increased as consumers dipped into their savings and saved a smaller share of their income. This is not unexpected given the decline in income due to the expiration of enhanced unemployment insurance. Wage and salary income continued to grow at a healthy pace and consumers continued to spend. However, their spending also continued to shift away from durable goods and toward services, which would be expected as the impact of the virus fades.

Here are the details: In September, total personal income fell 1.0% from the preceding month. However, wage and salary income increased 0.8%, partially offsetting a 7.0% drop in government transfers to individuals. After adjusting for inflation and taxes, real disposable personal income fell 1.6% from August to September. Yet real personal consumption expenditures increased 0.3%. This was facilitated by the savings rate falling from 9.2% in August to 7.5% in September.

The composition of spending was interesting. September was the fifth consecutive month in which real consumer spending on durable goods declined, this time by 0.5%. In fact, in the last five months real spending on durables fell 12.2%. Yet here is the interesting part: in September, real spending on durables was still 17.9% above the pre-pandemic level of February 2020. This huge demand for durable goods, even as it abates, is contributing to massive supply chain disruption and higher inflation. If spending on durables falls further, this can help to alleviate supply chain congestion and reduce inflationary pressure. Moreover, as people spend less on durable goods, they are spending more on services, something that should continue provided the virus stays in abeyance. Finally, it makes sense to spend less on durables. After all, how many big screen televisions, dishwashers, and treadmills can a family have in one home? That said, some of the decrease in spending on durables is due to troubles in the automotive industry, not due to lessening demand.

Meanwhile, real spending on non-durable goods increased 0.4% in September. Real spending on services was up 0.4%, the seventh consecutive monthly increase. However, despite strong growth in spending on services, real spending remains 1.7% below the pre-pandemic level of February 2020.

US inflation may have peaked, but wages accelerate

- Last week’s report on income and spending included the latest monthly data on the Federal Reserve’s favorite measure of inflation—the PCE-deflator. The overall PCE-deflator was up 0.3% from August to September and was up 4.4% from a year earlier. When volatile food and energy prices are excluded, the core PCE-deflator was up 0.2% from August to September and up 3.6% from a year earlier. The latter number was unchanged for the last four months, suggesting that underlying inflation might have peaked. A few more months of data might confirm this. Notably, the price index for durable consumer goods was up 7.3% from a year earlier while the price index for consumer services was up only 3.5% from a year earlier. This reflects the fact that inflation has been disproportionately due to supply chain stress in an overheated sector.

- Meanwhile, the US government released the latest employment cost index (ECI) which looks at the overall cost of employing workers, including both wages and benefits. The ECI was up 3.7% in the third quarter versus a year earlier. This was the biggest increase in compensation costs since 2004. Wages were up 4.2% while benefit costs were up 2.5%.

In addition, the ECI was up 1.3% from the previous quarter, the highest since records began in 2002. The gains varied by industry and by occupation. On a quarter-to-quarter basis, the ECI was up 1.4% for manufacturing, 1.6% for retail, 2.2% for financial services, and 2.5% for leisure and hospitality. There was a stunning 7.0% increase in the ECI for aircraft manufacturing. Nonetheless, the ECI was up a more modest 0.8% for government workers, 1.1% for transportation and warehousing, and 0.9% for wholesale trade.

By occupation, the quarterly ECI was up 1.5% for workers involved in production, transportation, and material moving. Meanwhile, it was up 1.0% for management, professional, and related occupations.

The acceleration in employment costs, especially wages, reflects the massive labor shortage that is vexing many businesses. Still, the increases in wages have not kept pace with rising prices. In other words, real wages have declined in the past year on average. If wages continue to rise at a rapid pace, this could contribute to sustained higher inflation. However, if businesses invest sufficiently in labor-saving or labor-augmenting technologies, then worker productivity gains can offset higher wage costs, thereby nullifying the necessity of raising prices.

What do investors think about US inflation?

One measure of investor expectations of inflation is the breakeven rate. Here is how it is calculated. The US Treasury (and other governments) issues two types of bonds: ordinary bonds that promise that the principal will be fully repaid and Treasury Inflation Protected Securities (TIPS; in the United States) that promise that the principal will move in line with inflation. Because investors are protected from inflation, the yield on TIPS is a real (inflation-adjusted) yield. Ordinary bonds provide a yield that, theoretically includes both the real return and investor expectations of inflation. Thus, the difference between the yields on ordinary and TIPS bonds is the investor expectation of inflation, also known as the breakeven rate.

In recent months, breakeven rates for five- and 10-year bonds have been rising as investors became increasingly worried about the potential for longer-term inflation. Still, breakeven rates have remained relatively muted, far below the actual inflation we have lately seen and reasonably close to the Federal Reserve’s target of 2.0% inflation. This likely reflected investor expectations that the current high inflation would turn out to be transitory. Indeed, the five-year breakeven rate has lately exceeded the 10-year breakeven rate, indicating that investors expect higher inflation in the short term than in the long term. This is consistent with the story that current inflation will be transitory. For some time, I and other economists have argued that, if breakeven rates suddenly spike, then investors will have become worried and will have upwardly revised their expectations, possibly compelling central banks to tighten monetary policy faster than anticipated.

In the past two weeks, breakeven rates started to spike. That is, they increased sharply, suggesting that the market zeitgeist is shifting as business leaders increasingly bemoan the apparent persistence of inflation. The supply chain problems in the global economy increasingly appear difficult to undo and the continuing rise in oil prices is a source of distress. Indeed, oil prices are now at the highest level since 2014. From October 19 through 22, the 10-year breakeven increased from 2.54% to 2.64%—a jump of 10 basis points and hitting the highest since 2006. The five-year breakeven increased from 2.71% to 2.91%, a jump of 20 basis points and hitting the highest since 2005.

Federal Reserve Chairman Powell was asked about this on October 22. Here is what he said: “The risks are clearly now to longer and more persistent bottlenecks, and thus to higher inflation. Supply constraints and elevated inflation are likely to last longer than previously expected and well into next year, and the same is true for pressure on wages. If we were to see a risk of inflation moving persistently higher, we would certainly use our tools.” He did not walk away from the transitory narrative. However, he appeared to suggest that the definition of transitory is a bit more prolonged than previously believed. He also attempted to reassure investors that the Fed is prepared to change course if things get out of hand.

Meanwhile, two-year US bond yields have risen sharply recently. These yields are a good proxy for investor expectations about short-term rates, which are controlled by central banks. Thus, a rise in the yield on short-term bonds suggests that investors expect the Federal Reserve to increase short-term rates sooner and by more than previously anticipated. In other words, investors evidently believe that the probability the Fed acts soon has increased, if only a little. Currently, the market is pricing in an increase in the Federal Funds rate late in 2022.

Finally, US equity prices have rebounded to a record high. If those who worry about stagflation are correct, equities should be sinking. What is happening? First, let’s define stagflation. Stagflation describes what happened in the 1970s when the economy was stagnant amidst unusually high inflation. Given that, historically, there has often (but not always) been an inverse relationship between growth and inflation (at least in the short term), stagflation is seen as perverse in that prices rise rapidly even amidst slow growth, and growth remains slow, even with significant inflationary pressure. That is not the case for now, at least not yet. The economy appears to be growing rapidly, with very strong consumer demand, something that is likely contributing to the current high inflation. Rising equity prices suggest that investors expect continued strong growth. Moreover, perhaps they recognize that inflation can often be good for corporate profitability as it reduces consumer sensitivity to price movements.

At the same time, perhaps investors expect inflation to ultimately fade, thereby allowing for continued low borrowing costs amid healthy growth. Indeed, an index of the prices of industrial metals fell sharply last week, suggesting that prices had previously overshot, or that shortages are starting to abate. Either way, this is evidence in support of transitory inflation. Finally, investors might be pleased that the yield on TIPS, which is the real, or after-inflation yield, has been falling into deep negative territory. That means that, after inflation, the cost of government borrowing is negative. That, in turn, is favorable for businesses that want to invest heavily.

[“source=deloitte”]