Housing finance companies (HFCs) are witnessing the most tumultuous time following the liquidity crisis that engulfed the non-banking finance sector (NBFC) since September 2018.

Over the past 5-7 years, HFCs have rapidly gained market share in the overall housing credit pie. The total housing finance market of around Rs 16.7 lakh crore as at March 31, 2018 has grown at a five year CAGR of 18 percent. The pace of growth of HFCs and NBFCs was higher than banks, at a five year CAGR of 20 percent. However, in the aftermath of liquidity crisis, the housing credit landscape is undergoing a change.

Most housing finance companies reported decent performance in Q3 FY19, despite the funding environment remaining constrained. Barring a couple of HFCs, which witnessed a sharp drop in loan growth, performance was decent for most HFCs across business parameters such as loan growth, spreads, asset quality and capitalisation.Liquidity easing not broad-based

While the liquidity situation has improved in the past couple of months, funding to HFCs has been very selective. HFCs with significant exposure to non-individual housing loans (loan against property, developer financing and construction financing) will find it most difficult to raise resources.

Hence, we remain extremely wary of HFCs that have a large proportion of non-individual housing portfolio. For instance, around 40 percent of Indiabulls Housing Finance’s (IBHF) book consists of non-individual housing book. While Housing Development Finance Corporation (HDFC), PNB Housing Finance and LIC Housing Finance also have varying proportion of non-individual housing loans at 30%, 43% and 6% of total book, respectively, their strong parentage comes to rescue and aids in raising funds at reasonable cost.

Funding has improved on increased portfolio assignments

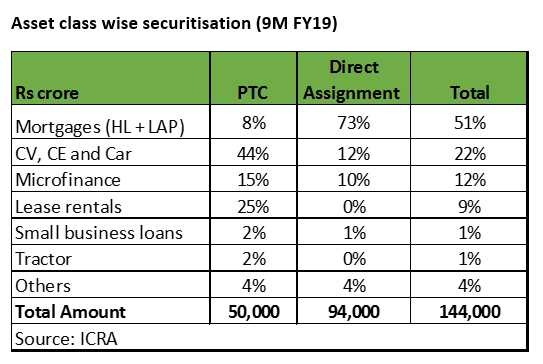

While conventional funding sources like commercial paper has reduced, HFCs are increasingly relying on portfolio selldown to banks. The latter too prefers buying the portfolio of HFCs as against direct lending to them. As a result, domestic securitisation market volumes have touched an all-time high of Rs 1.44 lakh crore during April to December FY19 as compared to market volumes of Rs 84,000 crore for the entire FY18, as per ICRA estimates. Mortgage-backed loans remained the most preferred asset class, accounting for 51 percent of total securitisation value in 9M FY19.

Most HFCs have resorted to direct assignment (DA) of the loan pool against pass through certificate (PTC) transactions as they can upfront book the income under Ind AS for loans sold through DA.

Growth to slowdown

Following the liquidity crisis, focus of HFCs has shifted from loan growth to conserving or raising liquidity. Many HFCs have increased rates on non-housing loan segment to raise liquidity through prepayments.

The overall growth of HFCs is likely to moderate in coming months. Also, the share of home loans in the overall on-book portfolio would also decline owing to increased retail portfolio sales by various HFCs.

IBHF’s loan growth in Q3 slowed to 16% as compared to 29% in Q2. The management guided that while total assets growth is expected to grow 20-25%, balance sheet growth will be around 10% for FY20 as it continues to sell down pools of loans.

Asset quality remains vulnerable

While the overall asset quality for HFCs has held up well so far, pressure is being seen in some pockets of housing credit. For instance, asset quality for the newer HFCs in the affordable segment (likes of Aspire Home Finance and Mahindra Rural Housing Finance) is significantly weak. Tightening liquidity and slowdown in growth could impact asset quality in segments like construction finance and LAP.

Profitability to moderate

The overall profitability indicators for HFCs remained healthy in Q3. However, going forward, a mix of factors could adversely impact earnings of HFCs.

HFCs, which have cruised on lower borrowing costs and easy access to finance in the past few years, are set for some hiccups as the cost of funds have risen. That said, large HFCs (assets above Rs 30,000 crore) accounting for around 80% of non-bank housing loan book are expected to remain more or less unscathed.

While most of the HFCs have increased their lending rates, it is extremely difficult to pass on the entire rate increase to borrowers in intensely competitive market. Hence, we anticipate pressure on margin and growth of HFCs.

While we don’t envisage the current liquidity issues to transforms into a credit crisis, there is likelihood of increased credit cost especially in non-housing portfolio, if the growth slowdown persists for longer.

Reduction in operating cost and upfront income booking on assignment transactions are likely to aid profitability.

Valuation and outlook

We are positive on the long-term growth prospects of HFCs. However, in the current scenario one should opt for a selective approach. While larger players will continue to dominate mortgage market, we see many small players ceding their market share in favour of banks.

Stocks of HFCs have nosedived following the funding concern. As such, valuations have turned reasonable. However, the investment decision in HFCs currently should be driven by asset mix. A HFC with granular retail assets, a relatively less risky book, is in a better position to raise funds. On the other extreme, wholesale financing HFCs are staring at a double whammy: risk of rising bad loans on asset side and difficulty in refinancing debt on the liability side.

Investors dumped the IBHF stock following the liquidity crisis. Despite a sharp price correction, valuation is not very enticing as its profit growth guidance has been pared down to 17-19% for FY20. Investor should avoid the stock.

Largecap names like HDFC should form part of investor’s core portfolio. LIC Housing also offers a lot of comfort, emanating from its strong parentage and reasonable valuations. Repco Home Finance should be on investor’s radar as the risk-reward has turned extremely favourable, with the stock currently trading at low valuation of 1.1 times FY20 estimated book.

Aavas has been clear outlier as the stock is up 62% in the last four months. High earnings growth and quality book in a rising affordable housing segment are reasons behind the strong rally. Long-term investors can buy the stock on dips.

In today’s environment, where access to funding has become a function of market confidence, we suggest investors to stay with large players with a strong parentage.

[“source=moneycontrol”]